Subscribe to the NTA’s Blog and receive updates on the latest blog posts from National Taxpayer Advocate Erin M. Collins. Additional blogs can be found at dev.taxpayeradvocate.irs.gov/blog.

In last week’s blog, we discussed how broad amnesties can blunt economic deterrence, but narrow amnesties or amnesty alternatives (e.g., amnesties that forgive only penalties before noncompliance is detected) do not necessarily have the same negative effects. We also cited research suggesting that those who participate in amnesties also tend to be people who made inadvertent errors (i.e., “benign” actors, rather than bad actors). Furthermore, without an amnesty, a sudden increase in penalties or enforcement is more likely to be viewed as unfair and erode trust for the government – a view that can erode voluntary compliance.

This week, we apply our findings to the IRS’s Offshore Voluntary Disclosure Programs (OVDPs). The IRS’s timing was right. It offered a series of OVDPs after Congress increased the penalty for failure to report foreign accounts on a Report of Foreign Bank and Financial Accounts (FBAR), and before the IRS was expected to receive more information from third parties about undisclosed accounts. However, the OVDPs were initially designed as a one-size-fits-all solution that was not a good option for those who typically participate in amnesties – benign actors who made inadvertent errors. While the OVDPs generated a significant amount of revenue – $11.1 Billion, according to the IRS – and probably avoided significant enforcement costs, the IRS’s initial failure to design programs for benign actors probably eroded trust for the IRS, posing risks to voluntary compliance, as discussed in my annual reports to Congress (2017, 2014, 2013, 2012, and 2011 (p. 206)).

The government’s relatively sudden shift – from virtually no enforcement before 2004 (as described by the Treasury Department here) to disproportionate penalties for those who made honest mistakes – did nothing to promote the view that it was reasonable or trustworthy. Indeed, one study projected that its 2009 OVDP increased tax evasion. Although the author speculated the increase was due to a negative effect on deterrence, it could have been due to the OVDP’s negative effects on the public’s trust for the IRS. The remainder of this blog describes these problems in more detail.

U.S. persons have long been required to report foreign accounts on a Report of Foreign Bank and Financial Accounts (FBAR). Before 2004 (when Congress increased FBAR penalties), however, the FBAR filing requirements were not well known, noncompliance was the norm, the requirements were rarely enforced, and violations were lightly punished. In 2002, the Treasury Department reported that the FBAR compliance rate could be less than 20 percent, and that it had imposed civil FBAR penalties in only 2 cases between 1993 and 2002.

Beginning in 2000, as part of its Offshore Credit Card Project (OCCP), the government used John Doe summonses to try to obtain the identities of U.S. taxpayers who held credit or debit cards issued by offshore banks on the suspicion that they were engaged in tax evasion (as described by the IRS and the Treasury Inspector General for Tax Administration (TIGTA), here and here). It also took steps to increase the automatic exchange of information with other countries (as discussed here). It proposed to collect more information about the earnings of nonresidents so that it could provide the information to other countries, entering into treaties containing Tax Information Exchange Agreements (TIEAs). (Congress ultimately passed FATCA in 2010, which requires even more third-party information reporting.) Thus, the IRS was increasingly able to identify people with unreported offshore accounts. When it examined the returns of those identified through the OCCP, however, it generally did not assess any additional tax, according to TIGTA. Beginning in 2003, the government offered a series of settlement programs, as discussed below.

Between January 14, 2003, and April 15, 2003, the IRS offered the Offshore Voluntary Compliance Initiative (OVCI) to persons using offshore payment cards or similar arrangements to improperly avoid paying taxes, provided it had not yet identified them. Participants would have to pay six years of back taxes, interest, and certain accuracy and delinquency penalties, but would not face any civil fraud or information return penalties (including FBAR). The OVCI might have reduced the costs of addressing noncompliance, but limits on who could participate, as well as the one-size-fits-all terms and the availability of better alternatives for many taxpayers – the qualified amended return (QAR) process and IRS’s longstanding criminal VDP – probably hurt its popularity. Moreover, it was not coupled with a visible increase in the risk of detection, except for John Doe summonses. A 2005 report by Treasury provided little reason to think that the government was changing compliance norms.

The IRS received about 1,326 OVCI applications and reportedly collected about $225 million, mostly from relatively compliant taxpayers. More than half of the OVCI applicants had reported their offshore income and paid taxes, but were merely rectifying the failure to file an FBAR, according to testimony by the General Accounting Office (now the Government Accountability Office or GAO). Even among those who owed tax, they owed a median of only $5,400, suggesting that an audit strategy might also fail to uncover significant tax noncompliance, unless it focused on those who did not participate.

Between 2003 and 2009, the IRS tried to settle cases by issuing letters to taxpayers who had been identified as holding an offshore payment card (or similar arrangement) to access an undisclosed account, offering them the so-called Last Chance Compliance Initiative (LCCI). This filled a gap left by the OVCI, which did not apply to those who had been identified. Under LCCI, the IRS would waive certain penalties for failure to file information returns and only impose the civil fraud and FBAR penalties for a single year, even if they could be applied to multiple years. Notably, it did not supplant the longstanding QAR or voluntary disclosure practice. Nor did it eliminate the option to settle on more favorable terms when warranted, according to CCA 200603026. Because the LCCI applied to those who had been identified, its primary purpose seems to have been to reduce the costs of the enforcement process. It was particularly important to have a way of reducing enforcement costs, as the OVCI data suggested that audits might not be worthwhile.

In 2004, Congress amended 31 U.S.C. § 5321(a)(5), imposing a new penalty for non-willful failures to file an FBAR and drastically increased the penalty for willful violations. This increase provided a unique opportunity for the IRS to promote compliance using a settlement program. In 2009, the IRS “strongly encouraged” anyone who had failed to file FBARs and similar returns reporting income from foreign accounts to participate in an offshore voluntary disclosure program (OVDP), according to FAQ #10. It discouraged them from using the longstanding QAR program. It warned that taxpayers making such “quiet” disclosures could be “criminally prosecuted,” while OVDP participants would generally be subject to a fairly-severe “offshore” penalty in lieu of various other penalties, including FBAR. Under the 2009 OVDP, taxpayers were required to pay:

The penalty rate would recover the present value of the unpaid tax on the accounts for the last 23 years, assuming the taxpayer earned 5 percent in interest that went unreported each year, according to GAO. Thus, the IRS circumvented the QAR process as well as the long-standing amnesty granted by Congress when it established a statute of limitations. Moreover, the IRS seemed to assume that its earlier programs had changed norms to such an extent that only intentional tax cheats were not complying with the rules, notwithstanding the fact that OVCI applicants had been a diverse group that included many with inadvertent violations.

The IRS expected those taxpayers who thought the offshore penalty was too severe to apply to the OVDP and then opt out. However, it warned in FAQ #34 that “[A]ll relevant years and issues will be subject to a complete examination … [and] all applicable penalties (including information return and FBAR penalties) will be imposed” [emphasis added] against those who opt out. This suggested that the IRS would seek the maximum penalty against people whose violations were not willful. OVCI data suggested that the IRS was bluffing because it would not have been a wise use of its resources to do so. However, the IRS’s message undermined trust.

While my office and external stakeholders were raising concerns about the 2009 OVDP and urging the IRS to disclose and retract a memo that reinterpreted key terms of the program (e.g., in connection with the National Taxpayer Advocate’s June (p. 23) and December (p. 206) reports to Congress, and in TAD 2011-1), the IRS established the 2011 Offshore Voluntary Disclosure Initiative (OVDI) (also referred to as an OVDP). (Note: As of March 13, 2108, the 2011 OVDI FAQs, which were absent from the IRS website for an extended period are now available here, due to TAS’s advocacy. See discussions here, here, and here, for our concerns about the IRS’s inappropriate use of FAQs, which can also undermine trust.)

After the 2011 program closed on September 9, 2011, it was succeeded by the 2012 OVDP, which was open ended, and the so-called 2014 OVDP which is a continuation of the 2012 program under slightly modified terms. The offshore penalty rose to 25 percent of the highest account balance during an eight-year period under the 2011 OVDP, to 27.5 percent under the 2012 OVDP, and up to 50 percent (still over an eight-year period) under the 2014 program. With a couple of extremely narrow exceptions, the 2011 OVDP applied the same offshore penalty to benign and bad actors. Fewer than two percent of the offshore penalties were assessed at the lower 5 percent and 12.5 percent rates.

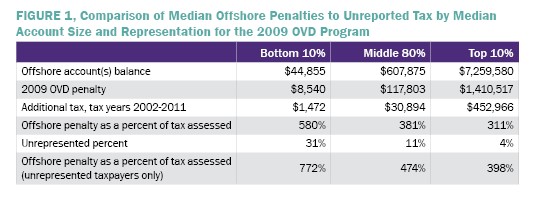

The only other option for benign actors was to opt out of the OVD programs and be examined. However, because those opting out faced prolonged uncertainty, the expense and stress of an examination, potential appeals, and the risk of even more severe penalties, some agreed to pay the offshore penalty designed for bad actors. Inside the 2009 OVDP, the median offshore penalty paid by those with the smallest accounts was nearly six times the median unreported tax, and unrepresented taxpayers generally paid even more – significantly more than represented taxpayers with the largest accounts, as shown below.

The IRS reported that as of October, 2016, 55,800 participants had paid more than $9.9 billion in connection with these programs, dwarfing the 2003 OVCI. This may have been due to the IRS’s increasing access to information about offshore accounts, Congress’ increase in FBAR penalties, widespread publicity, and the perceived lack of other options for taxpayers who inadvertently failed to report income from offshore accounts. But, for many taxpayers there was no evidence that penalties were warranted (and articles in the tax press suggested many were not) and the costs and long-term consequences are still unknown.

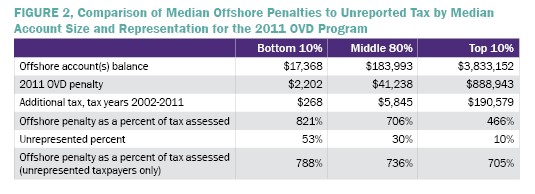

Perhaps because most of the taxpayers with significant offshore assets who wanted to participate had already done so and because the penalty rate increased under the 2011 OVDI, the disproportionality of the offshore penalty increased as a percent of tax assessed under the 2011 OVDI for all taxpayers, but especially for taxpayers with the smallest accounts, who paid over eight times the median unreported tax, as shown below.

Moreover, the participant’s accounts generally became smaller with each new program. This makes sense because the programs were not initially designed to attract middle-class taxpayers whose violations were not willful, but they were increasingly learning about the FBAR requirements, the potential for draconian penalties, and the IRS’s enforcement efforts, and were terrified. Thus, they came into the programs under fear of prosecution, despite the IRS’s previous lack of enforcement.

In the next blog, we will discuss how the IRS eventually provided more reasonable options for benign actors, and although the IRS announced on March 13, 2018, that it will discontinue the OVDP, we will also discuss how it could improve the program.

The views expressed in this blog are solely those of the National Taxpayer Advocate. The National Taxpayer Advocate presents an independent taxpayer perspective that does not necessarily reflect the position of the IRS, the Treasury Department, or the Office of Management and Budget.